What Institutional Capital Can Teach CEOs and Investors**

Executive Perspective

Banks are not emotional investors. They are disciplined, data-driven institutions whose survival depends on risk management, predictable returns, and long-term value preservation. When banks consistently allocate capital to specific asset classes, sectors, or structures, it sends a powerful signal: the model works.

Yet many private investors, business owners, and even CEOs hesitate to follow similar strategies—often waiting for “perfect timing” or chasing higher-risk alternatives. This raises a simple but critical question:

If banks do it, why don’t you?

This article explores how banks think, where they deploy capital, and why aligning parts of your investment strategy with institutional logic can significantly improve long-term outcomes.

1. How Banks Really Think About Money

Banks do not chase hype. Their capital allocation decisions are guided by three core principles:

1.1 Capital Preservation Comes First

Before returns, banks prioritize:

- Asset-backed security

- Predictable cash flow

- Downside protection

This is why banks favor assets such as:

- Real estate

- Infrastructure

- Cash-flow–generating businesses

High volatility may attract headlines, but it rarely attracts bank balance sheets.

1.2 Predictable Cash Flow Beats Speculation

Banks prefer:

- Stable income streams

- Long-term contracts

- Assets with recurring demand

They lend aggressively to sectors where cash flow can be modeled, stress-tested, and forecasted.

1.3 Time Is an Ally, Not an Enemy

Banks think in decades, not quarters. Compounding works best when capital is patient and consistently deployed.

2. Where Banks Put Their Money (and Why)

2.1 Real Estate and Property-Backed Assets

Banks finance and invest in:

- Commercial real estate

- Hospitality assets

- Mixed-use developments

Why? Because real estate offers:

- Tangible collateral

- Inflation hedging

- Dual upside (income + appreciation)

If a project were fundamentally weak, banks would not finance it at scale.

2.2 Hospitality and Hybrid Assets

Despite economic cycles, banks continue to support:

- Hotels

- Apart-hotels

- Condo hotels

These assets benefit from:

- Daily-rate pricing flexibility

- Tourism and business travel demand

- Professional management structures

Banks understand that well-located hospitality assets recover faster than most sectors.

2.3 Businesses With Recurring Revenue

Subscription-based and service-driven businesses attract bank capital because:

- Revenue visibility is high

- Customer behavior is measurable

- Risk is easier to price

Banks don’t bet on one-time wins—they invest in repeatability.

3. The Gap Between Institutional and Individual Investors

If the logic is clear, why don’t more individuals follow it?

3.1 Individuals Chase Upside, Banks Manage Risk

Private investors often ask:

“How much can I make?”

Banks ask:

“How much can I lose—and how do I control it?”

That difference alone explains most long-term performance gaps.

3.2 Emotion vs Systems

Banks operate with:

- Investment committees

- Credit scoring models

- Risk limits

Individuals often operate with:

- Gut feeling

- Market noise

- Short-term sentiment

Systems outperform emotions—every time.

3.3 Waiting for Perfect Timing

Banks rarely wait for “the bottom.” They:

- Enter gradually

- Structure downside protection

- Hold through cycles

Time in the market beats timing the market—especially for asset-backed investments.

4. What CEOs and Investors Can Learn From Banks

4.1 Follow the Capital, Not the Headlines

If banks continue to:

- Finance real estate

- Support hospitality assets

- Back infrastructure projects

It means fundamentals remain intact—even when sentiment fluctuates.

4.2 Think Like a Lender, Even When Investing

Ask the same questions banks ask:

- Is the asset income-generating?

- What protects the downside?

- Who manages the operations?

- How liquid is the exit?

If an asset cannot answer these questions, banks will avoid it—and so should you.

4.3 Structure Beats Speculation

Banks win not by guessing markets, but by:

- Structuring deals

- Limiting exposure

- Ensuring predictable returns

Smart investors adopt the same mindset.

5. Case Logic: Hospitality & Property Investments

Banks continue financing:

- Hotels in prime locations

- Mixed-use developments

- Condo hotels with strong operators

Why?

- People travel in good times and bad

- Cities grow, land becomes scarce

- Professional management reduces operational risk

If institutional capital is comfortable with long-term exposure, that confidence is not accidental.

6. Risk Is Not the Enemy—Unmanaged Risk Is

Banks do not eliminate risk. They:

- Price it

- Hedge it

- Structure around it

The lesson is not to avoid risk—but to control it intelligently.

7. The Strategic Question for Decision Makers

The real question is not:

“Is this investment risky?”

But rather:

“Is this the kind of risk banks are willing to take?”

If the answer is yes, the opportunity deserves serious consideration.

Conclusion: Think Institutional, Act Strategic

Banks survive because they respect fundamentals. They invest in:

- Real assets

- Cash flow

- Long-term demand

If banks continue to deploy capital into certain sectors, structures, and assets, it is not coincidence—it is strategy.

If the banks do it, the smarter question is not “why?”

It is:

Why aren’t you?

Word Count:

534

Summary:

Foreign currency trading is such a lucrative and easy to understand market that many who used to trade stocks, bonds, commodities and futures have switched to trading nothing but FOREX. Even Bill Gates and the world renowned trader Warren Buffet now trade currencies as part of their overall strategies. If they are doing it shouldn�t we follow them, after all isn�t it true that to become wealthy or successful you have to do what wealthy and successful people do.

Keywords:

FOREX, FOREX Trading, Currency, Currency Trading, Profits

Article Body:

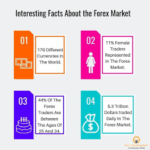

All major banks including central and government throughout the world make a �shed� load of money from the currency or foreign exchange market (FOREX).

In the year 2004 the Bank of America made over $750 million.

Until de-regulation in 1997, this money generator was only available to the large financial institutions, but now with as little as $300 any individual can open an account and trade FOREX.

Trading currencies is relatively unknown which is surprising because it is the largest market in the world (trillions of dollars are traded each and every day). It is the best trending market as it keeps moving in the same direction (this can be UP or DOWN) over 78% of the time. As there is no central exchange and because it is a world market FOREX can be traded 24 hours a day so it need not get in the way of your other business interests or social life.

Foreign currency trading is such a lucrative and easy to understand market that many who used to trade stocks, bonds, commodities and futures have switched to trading nothing but FOREX. Even Bill Gates and the world renowned trader Warren Buffet now trade currencies as part of their overall strategies. If they are doing it shouldn�t we follow them, after all isn�t it true that to become wealthy or successful you have to do what wealthy and successful people do.

You can make this market as exciting or as dull as you want, just turn the knob and you can have the adrenalin rush of jumping in and out of the market literally within seconds (commonly known as SCALPING, but we�re not playing cowboys and indians) or the more sedately approach of making your trade and then sitting back (this is known as INVESTING). Somewhere in between there is DAY and SWING Trading. It is entirely up to you which way you to trade or if you really want to go for it DO THEM ALL.

A word of caution, trading currencies may or may not be right for you but the good thing about this market is you can try it out. That�s right, you can open a demo or virtual account and do everything that you can do on a real account. But the really good bit is, it won�t cost you a dime.

Like everything else in life, from learning to crawl, to walking, to riding a bike, to swimming, to driving, and so on, you need to know what you are doing. Build your knowledge, study and practice, practice, practice.

Finally, once you know what you are doing and have proper money management skills, there is absolutely nothing to stop you becoming EXCEPTIONALLY WEALTHY as a result of trading foreign currencies.

I traded stocks when I first started but there were so many factors that you had to account for and so much to learn about each individual share and it�s company that it was a daunting and time consuming task. It was a very easy switch to trade currency.

I trade the FOREX market full time now and if you visit my website http://www.HomeForexTrading.com you can enrol on a FREE Trading course.

Tinggalkan Balasan